Emergency Fund 101

For those of us that have been on this earth long enough, we understand that life is like a cycle. Sometimes we’re thriving on top of the world and sometimes we’re fighting our way out of the trenches. Many experiences make a comeback, but all experiences (good or bad) have an end. Most would agree that one of the worst experiences in life’s cycle is an unpleasant financial surprise. Losing your job, totaling your car, inpatient hospital visits – once you come to terms with the fact that a financial setback is bound to happen to you, the real question becomes how can you weaken the strength of the next storm without knowing when it will come or how bad it will be? In the case of an unexpected financial crisis, the answer to that question is you need an emergency fund.

What Is An Emergency Fund?

As I’m sure you’ve guessed, an emergency fund is a pot of money set aside for financial emergencies. It’s important to understand what an emergency is and what constitutes as a financial emergency, though. An emergency, as defined by Oxford Languages, is “a serious, unexpected, and often dangerous situation requiring immediate action.” So, if an emergency fund should only be used for financial emergencies, then that means that it should only be used in situations that have a severe catastrophic impact on your life if an immediate action is not sought. A few examples of financial emergencies are:

Job loss

Medical or dental emergency

Unexpected home repairs (i.e., broken fridge, leaky roof, molded walls, etc.)

Car troubles (i.e., flat tires, totaled car, broken transmission, etc.)

Unplanned travel expenses (i.e., attending a funeral of a loved one in another state, etc.)

Where Should You Keep It?

Emergency funds should be held in accounts that are easily accessible, liquid, and not subject to market risk because it is money that you might need to withdraw in an extremely timely manner.

Let’s say for example that you lost your job and now must put yourself back in the job market, while maintaining your household’s financial responsibilities. If your money, was in a Certificate of Deposit (CD), you would have to pay a fee before you could withdraw your money from the financial institution that provided you the CD. If your emergency fund is in an individual stock market portfolio, that money would be subject to the cyclical highs and lows of the stock market (God forbid you lose your job during a recession when the stock market has crashed!).

When it comes to an emergency fund, I recommend housing it in a high-yielding savings account. Sure, a regular savings account or a checking account would be just fine, but since you’ll be stashing loads of cash into an account you won’t regularly access, you might as well earn a higher interest rate than the national average.

Whether you choose a high yield savings account or a regular checking/savings account, it is very important that you do 2 things:

Ensure that the account is insured by the Federal Deposit Insurance Corporation (FDIC), which is an independent federal agency that insures the deposits made in U.S. banks and protects the account older from the event of bank failures.

Put the emergency funds in a separate account that does not combine your emergency funds with any other personal funds. This creates an out-of-sight out-of-mind approach that prevents you from the temptation of tamping into this fund for non-emergency reasons. (I personally have my emergency fund in a high yielding savings account with an online bank that is different from all other banks I have money in).

How Much Should You Save?

Now that you understand the importance of an emergency fund and where you should keep it, it’s important to understand how much you should keep in it. We recommend the equivalent of three to six months’ worth of living expenses. At the same time, it is important to understand the difference between expenses you absolutely need to survive and expenses for things you really enjoy.

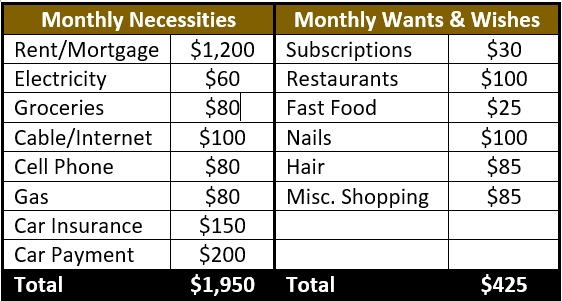

Let’s go back to our prior example of losing your job. How would you decide how much to save in an emergency fund? Well first you’d have to separate your monthly necessities from your monthly wants and wishes, like the chart below. Necessities would be things you need to survive and financial obligations for which you are already responsible. Wants and wishes would be things you enjoy doing but can do without for some time being. If your monthly budget were identical to the one below, we would recommend saving between $5,850 to $11,700 to cover three to six months of your monthly necessity expenses.

We also recommend reevaluating these figures annually, as your financial needs may change overtime (i.e., new home, newborn, new job, etc.). Additionally, we recommend replenishing your fund as soon as possible after tapping into it. You never know when your next financial storm will be!

How To Save For One?

Many people may feel intimidated by the amount they need to save for, especially if they must start from scratch. Our best advice to share is to build your emergency savings gradually by building it directly into your monthly budget. Set a reasonable goal for when you want to complete your emergency fund, as well as how much you can save monthly towards it. For most of us, that will mean cutting back on our monthly wants and wishes until we can fulfill our emergency fund goals.

Building off the example from above, let’s say we have a goal of $5,850 we want to save up for. We would start with re-evaluating the non-essential monthly expenses. Perhaps, we can cut out fast food and miscellaneous shopping fall together, and maybe we can cut our restaurants and nails budget in half. That leaves us with $210 that can now be allocated to an emergency fund. Which means that in about 2 years we would have satisfied our emergency fund requirements. That’s great news in the grand scheme of things! Especially, when you know that you can ask for cash for Christmas and your birthday, and you know that you may receive a tax refund check at some point during the year. You may even be able to negotiate your car insurance, car payment, cell phone, and cable/internet expenses down, which will help you lower the required figure for your emergency fund.

We recommend taking it a step further with automatic transfers into your designated emergency fund account. This will help you fight the temptation of spending that money, earn compounding interest on that money so that you may grow it faster, and keep track of your success towards your goals.

Whatever your strategy and however long (or short) it takes you, just remember that an emergency fund is a fundamental building block for financial stability and freedom. It is not a step to be overlooked or minimize. Just be reasonable, be strategic, be disciplined, and take your time. Slow and steady will win this race!